July 5 @ 9:00 am – 12:00 pm CDT Alexandria Farmers Market Big Ole Central Park 2nd Ave and Broadway Street, Alexandria, MN July 5 @ 4:30 pm – 8:00…Read More→

Paula Jackson

July 5 @ 9:00 am – 12:00 pm CDT Alexandria Farmers Market Big Ole Central Park 2nd Ave and Broadway Street, Alexandria, MN July 5 @ 4:30 pm – 8:00…Read More→

Staying at home in 2020 caused of lot of owners to think about how nice it would be to have a larger home to accommodate the additional activities that come…Read More→

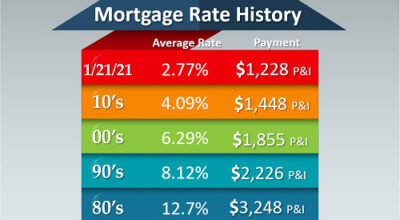

APR is the annual cost of a loan to a borrower including fees connected to the loan