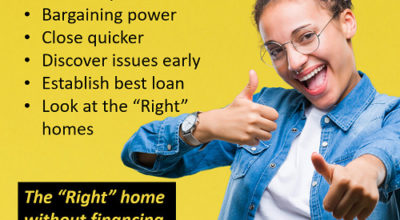

If you’re planning on buying a home in the next 3-6 months and isolating at home, now may be a good time to get pre-approved. You can do it online…Read More→

Paula Jackson

If you’re planning on buying a home in the next 3-6 months and isolating at home, now may be a good time to get pre-approved. You can do it online…Read More→

You don’t have to watch TV for long before Tom Selleck, Henry Winkler or Robert Wagner will tell you why seniors should consider a reverse mortgage. However, there are a…Read More→

The lint screen in clothes dryers should be cleaned after each cycle to improve its efficiency and reduce fire risk.

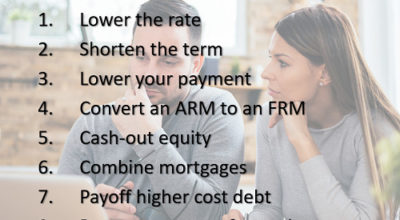

There can be several valid reasons that refinancing your home may be a good decision.