Skip to content

RE/MAX Results

Paula Jackson

My Listings

About Paula

Testimonials

Community

Alexandria

Douglas County

Minnesota

Osakis

Pope County

Todd County

Useful Links

Financing

Agency Disclosure

Buyer and Seller Tips

Interest Rates

Local Lenders

Mortgage Calculator

Your Home’s Value

Blog

Contact Me

Category: market updates

Would you move if it was to your advantage?

Posted on

January 8, 2021

January 8, 2021

by

admin

Home Inspections

Posted on

December 1, 2020

December 1, 2020

by

admin

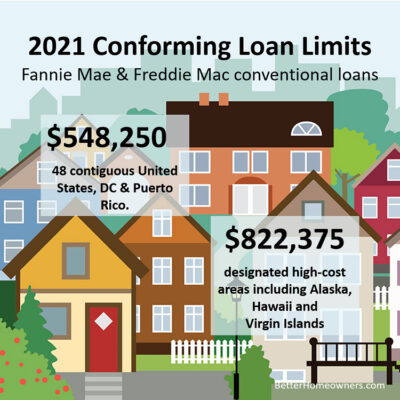

2021 Conforming Loan Limits

Posted on

December 1, 2020

December 1, 2020

by

admin

Vacation Sales Up

Posted on

November 20, 2020

November 20, 2020

by

admin

Posts navigation

Older posts

Enjoy this blog? Please spread the word :)