Skip to content

RE/MAX Results

Paula Jackson

My Listings

About Paula

Testimonials

Community

Alexandria

Douglas County

Minnesota

Osakis

Pope County

Todd County

Useful Links

Financing

Agency Disclosure

Buyer and Seller Tips

Interest Rates

Local Lenders

Mortgage Calculator

Your Home’s Value

Blog

Contact Me

Category: sales

Cutting Your Housing Costs in Half

Posted on

November 2, 2020

November 2, 2020

by

admin

Some Mortgage Interest May Not be Deductible

Posted on

October 27, 2020

October 27, 2020

by

admin

Alternative Investments

Posted on

September 28, 2020

September 28, 2020

by

admin

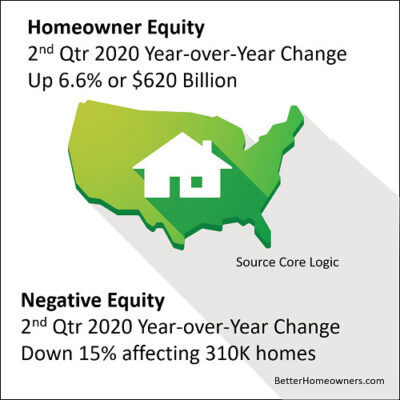

Homeowner Equity

Posted on

September 28, 2020

September 28, 2020

by

admin

Posts navigation

Older posts

Enjoy this blog? Please spread the word :)