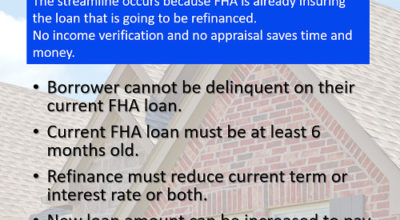

This streamline program is available for refinance situations because FHA is already insuring the loan. VA & USDA have similar programs.

Paula Jackson

This streamline program is available for refinance situations because FHA is already insuring the loan. VA & USDA have similar programs.

The American bank robber, Willie Sutton, was asked why he robbed banks and his answer was “because that is where the money is.” During his 40-year career, he stole about…Read More→

Safe at home is a perspective that can change attitude.